Debt-to-Income (DTI) ratio measures your monthly debt payments against your gross income. It’s critical as lenders use it to gauge your ability to manage payments and approve loans.

Understanding your Debt-to-Income ratio is essential for maintaining financial health. This ratio is a key metric that lenders evaluate to determine your creditworthiness. A lower DTI indicates to lenders that you have a good balance between debt and income, making you a less risky borrower.

This can increase your chances of getting approved for various forms of credit, including mortgages, personal loans, and credit cards. A higher DTI might signal financial stress, potentially leading to loan rejections or less favorable terms. Therefore, maintaining a DTI within acceptable limits is vital for anyone looking to finance large purchases or consolidate existing debts. Keep in mind that different lenders may have varying standards for what constitutes an acceptable DTI ratio.

Helping People Achieve Their Dream Of Homeownership!

👉 Simone Castello MLO (NMLS: 2181703)

📧 scastello@certifiedhomeloans.com

📞 WhatsApp No: +1 954-483-7742

Credit@ www.wellsfargo.com

Table of Contents

Decoding Debt-to-income Ratio

Debt-to-Income Ratio (DTI) stands like a financial health meter. Think of it as a scale that balances your debt against your income. Banks and lenders love DTI. It helps them say ‘yes’ or ‘no’ to loans. A good DTI means you can manage new debt. A high DTI? Not so good. It screams ‘risk!’ loud and clear. Now, let’s dive into DTI’s basics and how you can tally yours up.

The Basics of DTI

Think of your DTI as a pie chart. Your monthly debt slices up the pie. Your total monthly income is the whole pie. A smaller debt piece? That’s what you aim for. Credit cards, loans, and other ‘must-pay’ monthly bits add up to your debt. This ratio measures how much of your pie gets eaten up by these payments. A low DTI means a bigger piece of the pie stays with you. You get more financial flexibility and better loan chances.

Calculating Your DTI

Ready to calculate? Grab a calculator. Start with your monthly debts. Note each one on paper or a device. Include:

- Credit card payments, – Read How to Improve Your Credit Score

- Loans (car, student, personal, etc.)

- Mortgage or rent

- Any other regular payments

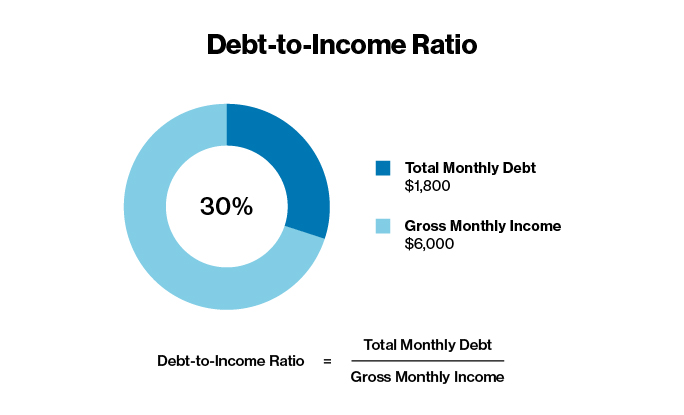

Next, jot down your total monthly income. This is what you take home. Now, it’s simple math. Divide your total debts by your total income. Move the decimal point two places to the right. Voilà, you have your DTI percentage.

| Step | Action | Result |

|---|---|---|

| 1 | List monthly debts | Total monthly debts |

| 2 | Note total monthly income | Total monthly income |

| 3 | Divide debts by income | DTI as a percentage |

Credit: mortgageone.com

Significance of DTI In Personal Finance

The Significance of DTI in Personal Finance cannot be overstated. DTI, or Debt-To-Income ratio, is a key indicator. It measures how much debt you have compared to your income. This ratio is crucial. Lenders look at it. It shows if you manage debt well. A good DTI helps in many ways. It can get you better loan terms. It shows financial stability. Knowing your DTI is the first step to financial health.

A Measure of Financial Health

Your DTI is like a financial health check-up. It tells you how much of your income goes to debt. A low DTI means more money for savings or spending. A high DTI signals you may have too much debt. It’s a sign to adjust your budget. Financial experts suggest a DTI below 36%. This is ideal. It helps keep your finances in green. Keeping track of your DTI helps avoid financial strains.

DTI’s Impact On Borrowing

DTI affects your ability to borrow money. Lenders use it to decide. A high DTI can limit your options. It might lead to higher interest rates. Or even loan rejections. Improving your DTI can open doors. It can lead to better loan offers. Here’s how:

- Lower DTI = Better Loan Chances. Lenders prefer lending to people with lower DTI.

- Competitive Interest Rates. A lower DTI often brings lower interest rates.

- Increased Borrowing Power. With a lower DTI, you might get a higher loan amount.

Keep your DTI in check. It’s important for loan success. Work towards reducing debt. Increase your income if you can. This will improve your DTI. Better DTI means better financial opportunities. Start by calculating your own ratio. Use this simple formula:

DTI = (Total Monthly Debt Payments / Gross Monthly Income) x 100Focus on this number in your personal finance journey. It’s a key to financial freedom.

DTI And The Mortgage Process

Understanding your Debt-To-Income (DTI) ratio is crucial when you’re looking to buy a home. This measure compares your monthly debt payments to your monthly income. Lenders use DTI to assess how comfortably you can manage a new mortgage. A lower DTI typically means a greater chance of loan approval. Let’s delve into how DTI affects the home buying journey.

Guidelines For Homebuyers

Lenders follow specific DTI guidelines. They generally prefer a DTI ratio of 36% or less. To break it down:

- Front-end DTI involves housing costs exclusively and should be under 28%.

- Back-end DTI includes all other debts and should not exceed 36%.

Some loan types may offer flexibility, with limits up to 43%. Aim for the lowest DTI possible when planning to buy a house.

Improving Your DTI For Loan Approval

Improving DTI is about increasing income or reducing debt. Here are proven strategies:

- Pay off smaller debts to decrease your total monthly payments.

- Avoid taking on new debts as you approach the mortgage application process.

- Consider a larger down payment to reduce the mortgage amount required.

- If possible, explore opportunities to boost your income.

Ensuring your DTI is in check is vital for a smooth mortgage process. Take steps to pare down debts and enhance your financial standing before applying for a home loan.

Managing High DTI Levels

Imagine your debt as a backpack you carry day-to-day. A high Debt-to-Income (DTI) ratio means your backpack is getting heavy. It’s stuffed with monthly payments right up to the brim. Managing high DTI levels is crucial, not just to lighten your load, but to secure financial health. It affects your ability to borrow money. Lenders use it to measure your monthly debt against your income. A lower DTI ratio means a lighter backpack, making life much easier.

Strategies To Lower DTI

Lighten your load with these deep-breath strategies:

- Pay more than the minimum on credit cards.

- Avoid new debt like a slippery banana.

- Increase income with side hustles or sales.

- Refinance loans for lower monthly payments.

Use a budget to track and trim monthly expenses. Knock off smaller debts first for quick wins. Consider debt consolidation. Stick to a plan to reduce your DTI gradually.

When To Seek Professional Help

If your debt feels like a mountain on your shoulders, it’s time. When monthly payments become overwhelming, don’t walk alone. A certified credit counselor can guide you through your options.

- Debt management plans.

- Credit counseling sessions.

- Debt settlement strategies.

A professional can provide a customized plan for your situation. They help negotiate with lenders and find the right path for you. Don’t wait for the backpack to break. Seek help when the load gets too heavy.

DTI’s Role In Financial Planning

Understanding your Debt-to-Income (DTI) ratio is like having a financial compass. It guides you through money decisions. A strong DTI opens doors to new opportunities. It shows lenders you’re a star at managing debt. Let’s dive into why it’s key for your wallet’s future.

Long-term Financial Stability

Sustaining your finances starts with a solid DTI. It measures monthly debt against income. A low DTI means you’ve got room to breathe. Banks smile when they see it. A healthy DTI suggests that you’re less risky. It’s a thumbs-up for financial freedom.

- Less strain on your budget – More cash stays in your pocket.

- Better borrowing power – Get loans with ease and better terms.

- Prepped for emergencies – Save with no worries about unwanted debt.

DTI For Investment Decisions

When picking investments, your DTI leads the way. A low ratio gives you wiggle room. You can snag investment deals without stress. A high DTI? That’s a red flag. Stay clear of adding more debt. Choose routes that help lower your DTI instead.

| DTI | Investment Approach |

|---|---|

| Low DTI | Flexible options, safe to take on some risk |

| High DTI | Focus on reducing debt, cautious investing |

Monitoring And Improving Your DTI

Monitoring and improving your Debt-To-Income (DTI) ratio is a savvy financial move. It highlights financial health. A strong DTI ratio can unlock loan approvals. It shows lenders you handle debt well. Keeping tabs on your DTI can mean better interest rates. It can also mean more borrowing power. Knowing and managing your DTI is key to financial success.

Regular Check-ups

Think of your DTI as a financial pulse. Taking it regularly makes sense. A quarterly review aligns with credit report checks. It flags any issues early. Spot changes in your debt or income quickly. Adjust spending or boost payments when needed. Maintain a DTI ratio lenders favor.

Tools And Resources For DTI Management

Numerous tools and resources can help manage your DTI. Online calculators provide quick checks. They measure your DTI in seconds. Budgeting apps track debts and income over time. They help make informed choices. Debt management plans are highly useful. They guide you toward a better DTI. Use these tools to stay on top of your finances.

A few key points to remember for DTI improvement:

- Decrease debt: aim to pay down loans and credit cards.

- Elevate income: seek ways to boost your earnings.

- Avoid new debt: think twice before taking on more.

Work on these areas consistently. Watch your DTI improve. Lenders notice these efforts. Financial flexibility can increase. Your creditworthiness gets stronger. Keep the aim: maintain a low DTI ratio for financial opportunities.

Credit: www.lendingclub.com

FAQ on What Is Debt-to-income (DTI)

What Is DTI And Why Is It Important?

DTI stands for Debt-to-Income ratio, measuring monthly debt payments against income. It’s crucial for lenders to assess borrowers’ ability to manage monthly repayments and overall debt risk.

Why Is The Debt-to-income Ratio Important?

The debt-to-income ratio measures your ability to manage monthly payments and repay debts. Lenders use it to assess creditworthiness and risk before granting loans. A lower ratio indicates better financial stability, enhancing loan approval chances.

Why Is DTI Useful?

DTI, or Debt-to-Income ratio, is key for assessing financial health. It helps lenders evaluate your borrowing risk and ability to manage monthly payments, influencing loan approvals and interest rates.

How Does DTI Affect The Customer?

A high DTI ratio may limit a customer’s loan options and result in higher interest rates. It can also restrict their ability to manage unexpected expenses.

Conclusion

Understanding your DTI ratio is crucial for financial health. It signifies credit risk to lenders and impacts loan approvals. Maintaining a low DTI ensures better loan terms and eases stress on your budget. Remember, a healthy DTI is key to a robust financial future.

Keep it in check for stress-free borrowing experiences.