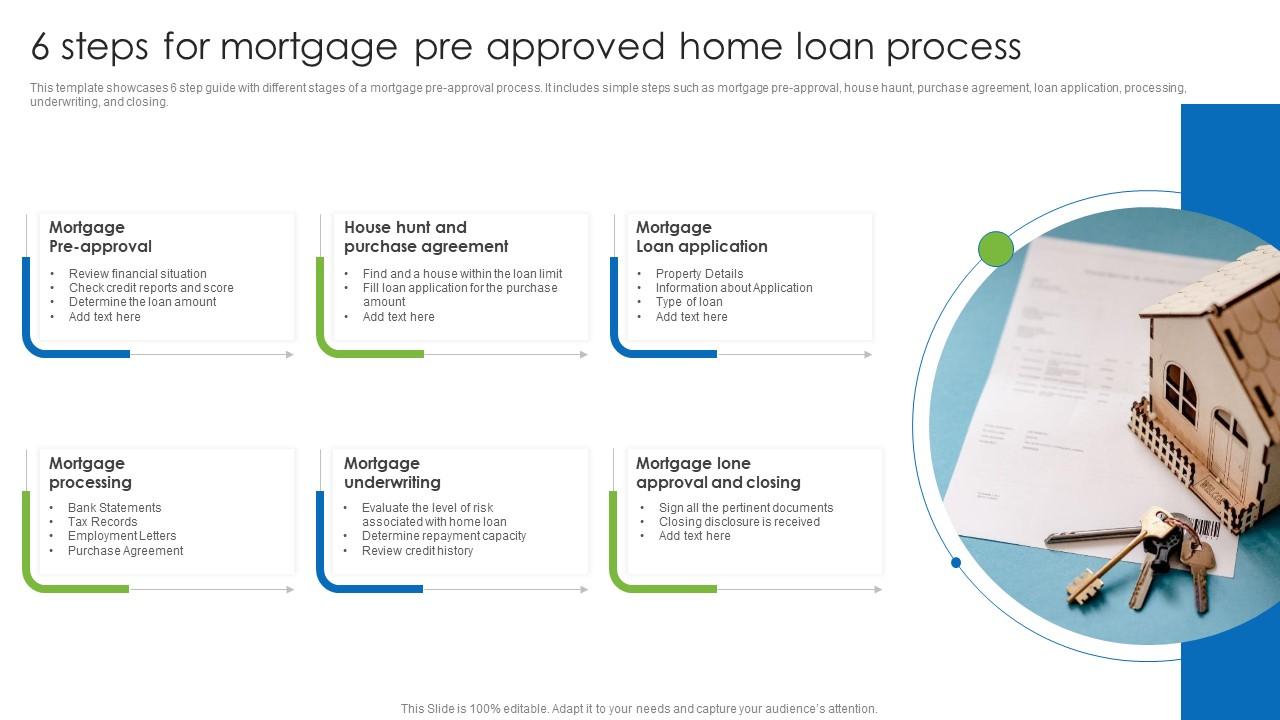

The mortgage loan process begins with a loan application and ends with closing. Borrowers must navigate credit checks, underwriting, and approval stages.

Securing a mortgage can be a pivotal step towards home ownership. The journey typically starts with a potential borrower completing a formal loan application, often after pre-qualification, which provides an estimate of how much they may borrow based on their finances.

Lenders then assess creditworthiness through a rigorous credit check and evaluation of financial documents. This review, known as underwriting, decides if the applicant meets the criteria for the loan. Upon a successful application, the next steps include receiving an approval, finalizing the loan terms, and proceeding to the closing, where the legal transfer of property and signing of documents occur. Understanding each component streamlines the experience, making the dream of owning a home a well-structured reality.

Credit: greatcoloradohomes.com

Table of Contents

Understanding Mortgage Basics

Embarking on the mortgage loan process requires a fundamental grasp of its structure, from pre-approval to closing. Homebuyers navigate through application, documentation, and finally secure financing for their dream property, marking each milestone with informed decisions.

Understanding the journey to homeownership begins with grasping the core elements of getting a mortgage. It’s like fitting together the pieces of a puzzle; each piece plays a critical role in seeing the big picture clearly. Let’s dive into the foundational aspects that can make or break your mortgage loan process.

What Is A Mortgage?

A mortgage is essentially a loan specifically designed for real estate purchases. Unlike most loans, a mortgage is secured by the property itself. This means if repayments aren’t met, the lender has the right to take ownership of the property through a process known as foreclosure.

Different Types Of Mortgages:

Before taking the plunge, it’s pivotal to know what suits your financial sea:

- Fixed-Rate Mortgage: A mortgage with an interest rate that remains constant throughout the life of the loan.

- Adjustable-Rate Mortgage (ARM): Features an interest rate that can change over time based on market conditions.

- Government-Insured Loan: Backed by the government, these loans include FHA, VA, and USDA loans, tailored to specific groups like first-time homebuyers or veterans.

- Conventional Loan:Not insured by the government, these require a higher credit score but often come with more flexible terms.

Principal And Interest

Embarking on the mortgage journey, the principal is the actual amount borrowed, while interest is the cost paid to the lender for borrowing that money. Over time, a portion of each payment reduces the principal, and the rest covers the interest—a process known as amortization.

Choosing The Right Mortgage For You

Finding the perfect mortgage is akin to selecting a partner for a long-term commitment. Scrutinize your finances and consider:

- Duration of Homeownership: Reflect on how long you plan to live in the home; this can influence whether a fixed-rate or adjustable-rate mortgage is more appropriate.

- Down Payment: Assess how much you can put down upfront, as this affects your loan amount and possibly your need for Private Mortgage Insurance (PMI).

- Your Credit: Your credit score will significantly influence the interest rates available to you, so check your credit report and score beforehand.

By familiarizing yourself with these mortgage basics, the path to obtaining a home loan becomes less daunting. Remember that it’s not just about finding a house; it’s about securing a foundation for your future—one that starts with a smart mortgage choice.

Preparation Phase

Embarking on the mortgage loan journey starts with thorough preparation. Essential in this initial phase is gathering documents like income verification, credit reports, and asset statements to ensure a smooth application process.

Embarking on the journey of acquiring a mortgage can seem daunting, but breaking it down into manageable phases can simplify the process. The preparation phase is the critical first step, setting the foundation for a smooth transition to homeownership.

Credit Score Assessment

Before diving into the vast sea of mortgage options, take a moment to evaluate your credit score. This three-digit number is a financial passport of sorts, opening doors to potential lenders and favorable interest rates:

- Understanding Your Score: Your credit score reflects your history with debt and payment, shaking hands with lenders ahead of time.

- Improving Your Score: Paying off outstanding debts and avoiding new credit applications shine a light on your financial responsibility.

Budget Planning

Knowing your budget inside out is like having a financial compass. Setting a price range that aligns with your income and expenses will ensure you’re not biting off more than you can chew:

- Income Analysis: Map out your revenue streams – this is pivotal in understanding how much you can allocate for monthly payments.

- Expense Tracking: Outline all current obligations and projected homeownership costs to avoid any monetary surprises down the road.

Gathering Necessary Documentation

Document collection can be as meticulous as gathering pieces of a puzzle. This includes:

- Proof of Income: Pull together recent pay stubs, tax returns, and W-2s, showing lenders that you have a steady stream of income.

- Asset Documentation: Summarize your assets, including savings, investments, and other properties that can act as a safety net for lenders.

Researching Mortgage Types

Your journey to finding the perfect mortgage is akin to trying on shoes – it’s crucial to find the right fit. Whether it’s a conventional loan, FHA, or VA loan:

- Loan Comparisons: Weigh the pros and cons of each loan type, factoring in your current financial landscape and future goals.

- Interest Rates and Terms: Understand how different rates and terms affect your monthly payments and total loan cost, which will be instrumental in making an informed decision.

Reaching Out To Loan Officers

Connecting with a loan officer is like seeking guidance from a financial sherpa – they’re there to help you navigate the complex mortgage terrain:

- Loan Officer Expertise: Their know-how can illuminate the path to the most suitable loan options and clarify any lingering questions.

- Pre-approval Potential: They can assist with a pre-approval, a green light that signals your readiness to sellers and gives you a competitive edge.

By diligently preparing for the mortgage loan process with these steps, you create a blueprint for success that can streamline your path to homeownership.

Choosing The Right Mortgage

Embarking on the mortgage loan process demands strategic decision-making. Selecting the right mortgage hinges on understanding terms, rates, and long-term financial impact, ensuring a decision that aligns with your financial goals.

Embarking on the journey to homeownership can often feel like navigating through an intricate labyrinth, where each turn presents a new decision to make. At the heart of this adventure lies the task of choosing the right mortgage—a critical step that can determine your financial flexibility and peace of mind for years to come.

Understanding The Types Of Mortgages

Before diving into the vast ocean of mortgage options, it’s crucial to have a clear map of the terrain. Essentially, mortgages come in various shapes and sizes, each tailored to different financial situations, housing markets, and long-term goals.

- Fixed-Rate Mortgages: These offer stability with the same interest rate and monthly payment amount throughout the entire loan term, ideal for those who crave predictability in their financial planning.

- Adjustable-Rate Mortgages (ARM): Characterized by an interest rate that may fluctuate over time, this option can suit those willing to trade a bit of uncertainty for the possibility of lower initial payments.

- Government-Insured Loans: Designed to lower the barrier of entry for homeownership, these include loans like FHA, VA, and USDA, which are backstopped by the government to protect lenders against defaults.

Evaluating Your Financial Situation

Identifying the best-fit mortgage becomes easier when you thoroughly evaluate your financial health and future aspirations. Let’s break down what you need to reflect.

- Credit Score: This number carries a lot of weight, influencing the kinds of loans you qualify for and the interest rates you’ll receive. A higher score unlocks more favorable terms.

- Down Payment: The upfront sum you’re able to put down not only affects your loan amount but can also impact your need for mortgage insurance and your monthly payment size.

- Budget: Outline your expenses and income to determine what monthly mortgage payment you can comfortably afford without stretching your finances too thin.

Looking At Mortgage Terms

The length of time you’ll be repaying your mortgage can also greatly influence your decision in selecting the most appropriate one. It’s about finding a balance between monthly payment amounts and total interest paid over the life of the loan.

- Short-Term Loans: Usually spanning 10 to 15 years, these can save you money on interest but often come with higher monthly payments.

- Long-Term Loans: With a typical duration of 30 years, they offer lower monthly payments but incur more interest over the loan’s lifespan, making it costlier in the long run.

Seeking Professional Advice

Making sense of the finer details of each mortgage option can feel daunting. This is where financial advisors or mortgage brokers step in to clarify doubts and provide tailored recommendations.

- They’ll assess your unique circumstances: A good professional will consider your financial status, goals, and risk tolerance.

- They help in streamlining the process: Their expertise can simplify comparing rates, terms, and fees, guiding you towards a decision that closely aligns with your objectives.

The selection of the right mortgage is a decision that reverberates through the fiscal structure of your life. With each step taken after careful consideration, you pave the way to a decision that is supportive of your life’s blueprint, ensuring that your financial foundation stands strong in the shifting sands of the economy.

Finding A Lender

Securing the right lender is a crucial step in the mortgage loan process. Thorough research and comparisons ensure favorable terms for your home financing needs.

Understanding Different Mortgage Lenders

Embarking on the journey to homeownership can be daunting, but finding the right lender is a crucial step. Different types of lenders cater to various buyer needs. With a spectrum ranging from large banks to online lenders, it’s essential to consider the size of the institution and the personalized services they offer.

Evaluating Lender Credibility

- Reputation: Research their standing in the industry and read customer reviews to gauge reliability and customer satisfaction.

- Loan Options: Evaluate their range of mortgage products to ensure they have a suitable option for your financial situation.

- Interest Rates and Fees: Compare their rates and fees with current market trends to ensure you’re getting a competitive deal.

- Customer Service: Consider the level of customer service and availability of loan officers for your inquiries and support needs.

Preparing To Meet Your Mortgage Lender

Before meeting with potential lenders, it’s wise to have your financial ducks in a row. This includes organizing your financial documents, knowing your credit score, and understanding your budget. A well-prepared borrower can make a strong impression and pave the way for a smoother loan process.

Helping People Achieve Their Dream Of Homeownership!

👉 Simone Castello MLO (NMLS: 2181703)

📧 scastello@certifiedhomeloans.com

📞 WhatsApp No: +1 954-483-7742

Navigating Loan Types And Terms

- Fixed-Rate vs. Adjustable-Rate: Decide if a stable monthly payment or the possibility of lower rates with potential rate changes fits your financial plan better.

- Loan Term Length: Analyze the pros and cons of different loan terms like 15-year or 30-year to determine what aligns with your long-term financial goals.

- Down Payment Requirements: Understand the implications of different down payment sizes on your monthly payments and mortgage insurance necessities.

Grasping The Importance Of Pre-approval

Securing a pre-approval from a lender is more than just an estimate of what you can afford; it’s a powerful tool in home buying. It signals to sellers that you are a serious buyer and can give you an edge in a competitive market, where making a swift and backed offer can make all the difference.

Comparing Lenders: The Final Step

- Loan Estimates: Request loan estimates from multiple lenders to thoroughly compare costs and fees side by side.

- Communication Style: Ensure the lender communicates in a manner that suits you, whether through digital channels or traditional methods.

- Closing Time Frames: Verify how long their loan closing process usually takes to align with your home purchase timeline.

By considering these crucial factors and keeping in line with your financial objectives, you’ll be well on your way to selecting a mortgage lender that not only fulfills your needs but also supports your journey to owning your dream home.

Applying For A Mortgage

Embarking on the mortgage loan process requires meticulous preparation and understanding of financial documents. Navigating the steps of securing a mortgage can facilitate homeownership dreams, ensuring a smoother transaction from application to approval.

Embarking on the journey of acquiring a home loan can feel overwhelming, but understanding the application process can equip you with confidence. Here, we’ll dissect each step, ensuring you know precisely what to expect.

Overview Of Mortgage Application Process

Securing a mortgage requires preparation, accuracy, and patience. Your first step involves gathering necessary financial documents and deciding the appropriate time to engage with lenders. Ensure you understand your credit score, as it significantly influences the loan terms you’ll receive.

Research different mortgage providers for competitive rates and reasonable fees to ensure you make a wise decision.

Documents Required For Mortgage Application

Before diving into applications, it’s important to have all your paperwork in order. Here’s what you’ll need:

- Proof of income: This includes recent pay stubs, tax returns, and any additional income documentation.

- Asset information: Bank statements and investment account statements to prove that you have funds for the down payment and closing costs.

- Personal identification: A government-issued ID and Social Security number are necessary to verify your identity.

- Employment verification: Lenders will want proof that you have a stable job and reliable income.

- Credit information: You should be aware of your credit score and credit history as lenders will use these to assess your loan eligibility.

Steps In Completing The Application

When it’s time to fill out your application, careful attention to detail is key. Here’s what the process generally looks like:

- Complete the application form: This includes personal information, financial details, and information on the property you wish to purchase.

- Submission of documents: Send in all the required documentation we listed earlier to your lender.

What To Expect After Submitting Your Application

Once your application is submitted, the waiting game begins. The lender will review your application, run a credit check, and authenticate your financial background. They may reach out for additional documentation or clarification, so keep your phone nearby and check your email regularly.

You’ll eventually receive a loan estimate document that outlines the costs associated with the loan; be sure to review this carefully.

Tips For A Smooth Application Process

By adhering to these tips, you can ensure a smoother application process:

- Maintain a healthy credit score: A good credit score could result in better interest rates and loan terms.

- Stay organized: Keep your documents and finances in order so that you can access anything requested by the lender quickly.

- Be prompt with responses: If your lender reaches out for more information, provide it as soon as possible to keep the process moving.

By following these structured steps and prepared with the right information, you’re setting yourself up for a more straightforward, transparent mortgage application process. It’s not just about taking the right actions but also timing them well to make your dream of homeownership a reality.

Mortgage Underwriting

Mortgage underwriting is a pivotal step in securing a home loan, where lenders assess the risk of lending to a borrower. An underwriter scrutinizes credit history, income, assets, and property value to ensure repayment capability and compliance with lending criteria.

Embarking on the journey of securing a mortgage can seem like navigating through an intricate maze. Central to this process is the phase where the magic behind the scenes unfolds:. This step is the financial heartbeat of your mortgage application, ensuring your dream home doesn’t slip through the fingers.

What Is Mortgage Underwriting?

Mortgage underwriting is the forensic analysis undertaken by lenders to determine if a borrower’s loan application is an acceptable risk. Beyond assessing creditworthiness, underwriters scrutinize income, assets, and the property in question—meticulously verifying the borrower’s capability to uphold their mortgage payments.

The Role Of An Underwriter:

- Assessing Creditworthiness: An underwriter meticulously reviews credit scores and history to evaluate the likelihood of timely repayments.

- Income Verification: They confirm income stability and reliability, ensuring borrowers have the means to fulfill payment obligations.

- Asset Evaluation: Underwriters examine bank statements and other assets to assure sufficient funds for down payments, closing costs, and financial reserves.

Automated Vs. Manual Underwriting:

With the dawn of the digital age, underwriting has bifurcated into automated and manual processes, each with unique advantages. Automated underwriting systems (AUS) can quickly evaluate applications against predetermined criteria, offering speed and consistency. On the flip side, manual underwriting allows for human judgment and flexibility, particularly for applications that don’t fit into the conventional boxes.

Conditions For Final Approval:

Once an underwriter greenlights an application, certain conditions typically follow—each a stepping stone toward final approval. This may range from providing additional financial documentation to clarifying discrepancies that may have surfaced during the underwriting process. Final approval signals the culmination of rigorous scrutiny, inching borrowers one step closer to homeownership.

Common Underwriting Outcomes:

The outcome of mortgage underwriting can fall into three main categories:

- Approved: Congratulations! The lender is satisfied with the risk and your application has been approved.

- Suspended: The underwriter requires more information before making a decision. This isn’t a denial, but rather a call for further documentation or clarification.

- Denied: Rejection can be disheartening, but understanding the rationale behind it is key to reevaluating your position and potentially reapplying in the future.

Mortgage underwriting might seem daunting, but it’s a testament to the thoroughness that underpins a secure and responsible loan. Managing this step with knowledge and preparation can set the stage for successful homeownership. Remember, a well-informed borrower is an empowered borrower, so take this insight as your torch to illuminate the path forward in the mortgage loan process.

Home Appraisal And Inspection

A crucial step in securing a mortgage loan is the home appraisal and inspection process. It assesses a property’s value and condition, ensuring lenders and buyers are well-informed before finalizing the loan.

Embarking on the journey of securing a mortgage loan, one encounters numerous milestones, each critical to the path leading to homeownership. Two such pivotal steps are the home appraisal and inspection, offering reassurances to both the lender and buyer about the property’s value and condition.

Home Appraisal

The home appraisal serves a dual purpose: it protects the lender’s investment by ensuring the property is worth the loan amount, and it gives buyers peace of mind about their prospective purchase. An appraiser, who is a licensed professional, conducts this assessment based on several factors:

- Location: The property’s geographical area influences its market value.

- Recent sales: Comparable sales of homes in the area often guide the appraiser’s valuation.

- Home condition: The state of the property, including updates and renovations, plays a significant role in determining its worth.

- Features: Number of rooms, layout, and any unique characteristics can affect the appraisal.

Home Inspection

Contrasted with the appraisal, a home inspection delves deep into the nuts and bolts of the property. It’s about uncovering hidden issues that could affect livability or cause future financial strain. The home inspector is charged with conducting a thorough examination, and here’s what it entails:

- The inspection covers a wide array of home elements, from the foundation to the roof.

- It can identify whether the electrical, plumbing, and HVAC systems are up to code.

- The condition of the home’s interior and exterior, including windows, doors, and insulation, is thoroughly evaluated.

- Pest infestations or damage, which can greatly impact the property’s integrity, are also on the checklist.

- Finally, a comprehensive report provides the buyer with a detailed account of the findings, often influencing the negotiation and purchasing process.

Navigating through the complexities of a home appraisal and inspection can indeed be daunting. Yet, armed with knowledge and understanding of their implications, buyers can make informed decisions, ensuring the investment in their future home is sound and secure.

Closing The Deal

Sealing the mortgage loan deal signifies the final step in homebuying. This crucial phase involves signing paperwork, finalizing terms, and ensuring legalities are in order, leading to the transfer of property ownership.

Embarking on the journey of finalizing a mortgage can often feel overwhelming, but understanding the ” phase can make this last hurdle a smooth and celebratory transition into homeownership. Read on to learn about the vital steps to seal the deal on your property.

Reviewing Closing Documents

It’s essential to scrutinise all the closing documents before you put pen to paper. Here’s what you should check with a keen eye:

- Loan Estimate and Closing Disclosure: Ensure consistency in the figures listed and clarify any discrepancies.

- Mortgage Note: This is your promise to repay the loan—confirm the interest rate, loan amount, and payment schedule.

- Deed of Trust: This gives your lender a claim against your home if you default on the mortgage. Make sure you understand the terms.

Final Walk-through

A final walk-through ensures everything is as agreed upon in your contract. It’s your last chance to:

- Confirm that any requested repairs have been made.

- Check that the condition of the home has not deteriorated since your last visit.

- Ensure all fixtures and appliances that were included in the sale are present and in working order.

Clearing Any Remaining Funds

Before you claim the keys, there are usually some financial loose ends to tie up. This may involve:

- Closing Costs: Covering fees for lenders and third-party services.

- Down Payment: The portion of the home’s price not covered by your mortgage.

Setting The Closing Date And Time

Choosing the right closing date can provide financial advantages, such as:

- Prorated interest: Closing later in the month can reduce the amount of interest due at closing.

- Strategic timing: Align the closing with your financial readiness and move-in timeline.

Understanding The Role Of Title Insurance

Title insurance is a safeguard against future claims and hidden issues, protecting you from:

- Previous legal claims or liens against the property.

- Any undiscovered issues that could challenge your ownership.

Signing The Papers

Finally, the moment has arrived to make your homeownership official:

- Come prepared with a government-issued photo ID.

- Expect to sign several documents—a notary will likely be present to officiate.

- Once all the paperwork is signed and funds are transferred, you’ll receive the keys to your new home.

Remember, every signature is a commitment. Don’t hesitate to ask questions if there’s something you’re unsure about. Being informed and clear during this concluding step of the mortgage loan process is the best way to transition confidently into your new home.

After Closing

After the final documents are signed, the mortgage loan process reaches the “After Closing” stage. This crucial phase involves recording the deed, disbursing funds, and ensuring that the new homeowner receives the keys.

Securing a mortgage and finally closing on your dream home is indeed an accomplishment worth celebrating. The keys are in your hand, and your heart is ablaze with excitement. Yet, even after the documents are signed and the last handshake is exchanged, the journey is not entirely over.

Let’s explore what follows after the grand milestone of closing your mortgage loan.

Post-closing Document Review

After the ink has dried on your closing documents, it’s crucial to conduct a thorough post-closing review to ensure everything is in order. This involves:

- Reviewing all closing documents: Ensure that the names, loan amount, interest rates, and terms match what was agreed upon.

- Understanding your payment schedule: Keep track of when mortgage payments are due to avoid any penalties.

- Confirming the deed recording: Check that the deed to the property has been officially recorded with the county.

Setting Up Mortgage Payments

Successfully managing your mortgage payments is the next significant phase post-closing. To mitigate any future financial confusion, you need to:

- Establish an escrow account if required: This account will handle property taxes and insurance automatically.

- Choose a payment method: Decide whether you want to pay by mail, online, or set up automatic withdrawals.

Maintaining Records And Documents

It’s not merely about keeping documents stashed away; it’s about knowing what they signify for your homeownership journey. Remember to:

- Safeguard important paperwork: Keep your closing package, loan documents, and warranties in a secure location.

- Stay on top of taxes and insurance: Understand your obligations and ensure these bills are paid on time to avoid any liens on your property.

Understanding Tax Implications

Homeownership brings with it a new set of considerations when tax season rolls around. It’s critical to know how your mortgage will impact your financial landscape:

- Review potential deductions: Mortgage interest and property taxes could provide worthwhile deductions.

- Keep receipts for home improvements: Some upgrades may qualify for tax credits or deductions.

Expecting The Unexpected

The future is unpredictable, and as a homeowner, being prepared for any curveballs is essential. This section underlines a few situations you might encounter:

- Anticipating maintenance and repairs: Houses require upkeep; set aside a budget for unexpected repairs.

- Being aware of loan servicing transfer: Sometimes lenders transfer the servicing of your loan to other institutions; pay attention to any notifications regarding this.

Embracing homeownership is not just about signing papers; it’s an ongoing commitment. Staying attentive and proactive after closing will help you navigate the post-loan process smoothly and maintain peace of mind. From keeping diligent records to understanding the nuances of tax implications, consider these steps your roadmap to managing your new property effectively and reaping the full benefits of homeownership.

Tips For A Smooth Mortgage Process

Simplify your mortgage loan process by gathering financial documents early and maintaining good credit. Choose a reputable lender, understand all terms clearly, and respond promptly to requests for information to ensure a smooth transaction.

Navigating the mortgage loan process can be a complex journey. From application to approval, every step is crucial to ensuring a positive outcome. Here’s how you can streamline the process for a quick and hassle-free experience.

Get Your Financial Documents In Order

Before diving into the mortgage process, prepare by collecting all necessary financial documents. Doing this early will save you time and demonstrate your credibility as a borrower.

- Proof of income: Include your W-2 forms, pay stubs, and tax returns from the past two years.

- Credit history: Obtain a copy of your credit report to review and address any discrepancies.

- Asset documentation: Compile statements from bank accounts, retirement funds, and other assets that verify your financial stability.

Understand Your Budget Limits

Clearly understanding your financial limits is key to ensuring a mortgage that you can comfortably afford.

It’s not just about the price of a new home; it’s about how this expense fits into your broader budget. Consider both the upfront costs, like down payment and closing fees, and ongoing expenses, including homeowners’ insurance, property taxes, and maintenance.

Pre-approval Is Golden

One significant step towards a smooth mortgage process is securing a pre-approval from a lender.

- Confidence booster: A pre-approval letter can elevate your status in the eyes of sellers, showing you’re ready to purchase.

- Budget clarity: This will give you an exact picture of how much you can borrow, refining your house-hunting efforts to properties within your means.

Keep Communication Lines Open

Prompt and clear communication with your lender will facilitate a smoother mortgage process.

Every query from your loan officer is an important piece of the puzzle. Respond swiftly to requests for additional documentation, questions about your credit history, or explanations of deposits in your accounts. Your cooperation is pivotal to advancing the process without delays.

Consider Loan Types And Terms

Explore the various types of loans and terms to find the one that best fits your long-term financial goals.

Choosing between a fixed-rate and an adjustable-rate mortgage impacts your financial planning over the duration of the loan. Similarly, decide if a 15-year loan with higher monthly payments but less interest over time makes more fiscal sense than a 30-year loan for your budget.

Anticipate Closing Costs

Closing costs can often be a surprising expense for many homebuyers. Anticipating these fees will prevent last-minute financial stress.

- Appraisal fees: Paid to the professional assessing the home’s value.

- Title search: Covers the due diligence to ensure the property’s title is free and clear of issues.

Stay Patient And Flexible

The loan process can sometimes include unexpected hurdles and delays.

Whether there’s a backlog in the lender’s pipeline or an appraisal comes in lower than expected, keeping a patient mindset and being flexible to provide additional information or make decisions can make the experience less stressful. Remember that most obstacles can be overcome with a calm approach and cooperative action.

With these tips in practice, your journey through the mortgage loan process should lead to a successful and satisfying home purchase. Stay informed, stay prepared, and keep the lines of communication open for the best results.

Common Pitfalls To Avoid

Navigating the mortgage loan process demands attention to detail to avoid costly missteps. Essential tips include maintaining a sturdy credit score, having consistent income documentation, and understanding all the terms and fees before signing any agreements. These proactive steps help dodge common errors that can derail home financing.

Embarking on the journey of securing a mortgage can be both exciting and daunting. As you navigate through various steps, there are several pitfalls you would do well to avoid to ensure a smooth and efficient process. Awareness and preparation can make a significant difference in acquiring your dream home without unnecessary hiccups.

Incomplete Documentation

One key to a successful mortgage application is providing complete and accurate documentation. Ensure you have all necessary documents before commencing:

- Proof of income: Includes tax returns, W-2 forms, and recent pay stubs.

- Credit history: Details of your credit score and any outstanding debts.

- Asset information: Bank statements and investment records that verify your financial stability.

Misunderstanding Loan Options

Understanding the different types of loans is crucial:

- Fixed-rate vs. Adjustable-rate: Know the pros and cons, fixed-rate offers stability while adjustable can initially be lower.

- Conventional vs. Government-insured: Conventional loans might require a higher down payment compared to FHA or VA loans.

Ignoring Credit Score

Your credit score plays a fundamental role in the loan approval process and the interest rates offered:

- Regular checks: Consistently monitor your credit report for accuracy and fraud.

- Improve your score: Pay off debts and keep credit utilization low to elevate your creditworthiness.

Underestimating The Total Cost

Owning a home goes beyond just the mortgage payment:

- Additional expenses: Property taxes, insurance, maintenance, and utility bills should be factored into your budget.

- Closing costs: Often overlooked, they can add up to a substantial amount. Save accordingly.

Switching Jobs Or Making Large Purchases

Stability is key when applying for a mortgage loan:

- Job consistency: Lenders prefer a steady employment history. A new job might delay or jeopardize your loan approval.

- Big-ticket purchases: These can alter your debt-to-income ratio. Postpone any major buys until after closing.

Overlooking Pre-approval

Securing pre-approval can give you a competitive edge:

- Clear picture: It outlines what you can afford, showing sellers you’re a serious buyer.

- Negotiation power: Pre-approval may give you room to negotiate better terms.

Neglecting To Compare Offers

Shopping around could save you thousands:

- Multiple lenders: Gather offers from various sources to ensure you’re getting the best deal.

- Read the fine print: Details matter. Ensure there are no hidden fees or clauses that could affect you later.

By being mindful of these common pitfalls and conducting thorough research, you can confidently move forward in the mortgage process. Your attention to detail and proactive approach will help pave the way to your new home with minimal stress. Remember, patience and preparation are your best allies in this significant financial decision.

The Future Of Mortgages

The mortgage loan process is evolving rapidly, leveraging technological advances to streamline applications and approvals. Future homebuyers can anticipate a faster, more intuitive path to securing their dream homes, thanks to digital innovations simplifying documentation and decision-making in the mortgage landscape.

The landscape of home financing is undergoing an exciting transformation, influenced by technological advancements and evolving consumer expectations. The mortgage industry is poised to become more accessible, efficient, and user-friendly. This direction not only promises to reshape the experience for homebuyers but also stands to redefine the operational structures of lenders.

Technological Innovations In Mortgage Processing

Embracing technology is at the heart of the mortgage sector’s future. Here are key innovations set to revamp the mortgaging experience:

- Automation: Lenders are increasingly implementing automated systems to streamline the application and underwriting process, leading to faster approval times and reduced paperwork.

- AI and Machine Learning: Artificial intelligence and machine learning algorithms are refining risk assessment capabilities, ensuring more accurate pricing and tailored loan offerings.

- Blockchain: This technology offers secure and transparent record-keeping, which could virtually eliminate fraud and errors in loan documentation.

Enhanced Consumer Experience

The next wave of mortgage processes will heavily focus on the borrower’s journey. Expect these enhancements:

- Personalized Service: With data analytics, mortgage providers will offer customized advice and solutions, effectively meeting unique borrower needs.

- Mobile-first Approaches: A surge in mobile applications for mortgage management reflects the industry’s adaptation to the convenience desired by consumers.

- Self-service Options: New platforms will empower consumers to manage their application, documentation submission, and status checks independently, without the constant need for direct lender interaction.

Sustainability And Ethical Lending

Moving forward, the ethical implications and sustainability of lending practices are becoming crucial considerations:

- Green Mortgages: Favorable loan conditions for energy-efficient homes are not just a niche product anymore but are becoming a mainstream offering.

- Responsible Lending: There’s greater pressure for transparency and fairness in lending, with regulations steering the industry toward practices that truly serve the best interests of borrowers.

Remote Notarization And Closing

Signing on the dotted line is getting a digital upgrade. Behold the changing closing ceremonies:

- Electronic Notarization: Remote, electronic notarizations save both time and resources, allowing for a legally-binding process to occur from anywhere.

- Digital Closing Rooms: Virtual spaces for closing transactions are being tailored to maintain the significance and security of the final step in the mortgage process.

These advancements demonstrate that the future of mortgages is not just a rehash of the old system adorned with new tools—it’s a complete ground-up reimagining that elevates every touchpoint into a smarter, smoother, and more consumer-friendly journey. By staying abreast of these developments, borrowers and lenders alike can navigate the mortgage process with greater ease and confidence in the years to come.

Credit: www.slideteam.net

Frequently Asked Questions for Mortgage Loan Process

What Are The Steps In The Mortgage Loan Process?

The mortgage loan process involves five key steps: pre-approval, home shopping, mortgage application, loan processing, and closing.

What Is The Procedure To Get Mortgage Loan?

To get a mortgage loan, start by reviewing your credit score. Next, gather necessary financial documents. Then, choose a suitable lender and apply. Compare loan offers carefully. Finally, proceed with the loan approval and closing process.

How Long Does It Take For A Mortgage Loan To Be Approved?

A mortgage loan approval can take as little as a few days or up to several weeks. The typical timeframe is about 30 days. Delays may occur with complex situations or document verification.

What Happens Once My Home Loan Is Approved?

Once your home loan is approved, you will receive a formal approval notification. Next, sign the loan documents, arrange insurance if necessary, and the lender will then disburse funds to finalize the property purchase.

Conclusion

Navigating the mortgage loan process can seem daunting, yet it’s a path to homeownership. We’ve demystified each step to empower you with knowledge. Remember, preparation and understanding are key to a smooth journey. With the right guidance and resources, your dream home is within reach.