When it comes to loans, understanding the terms can seem tough. Two key terms are Note Rate vs Annual Percentage Rate (APR). We’ll explain what they are and how these rates impact your loans and mortgages.

Helping People Achieve Their Dream Of Homeownership!

👉 Simone Castello MLO (NMLS: 2181703)

📧 scastello@certifiedhomeloans.com

📞 WhatsApp No: +1 954-483-7742

Table of Contents

Note Rate

The Note Rate is the actual interest rate on a loan. This is the rate used to calculate your monthly payments. It does not include other costs.

Annual Percentage Rate (APR)

The APR, however, includes the note rate and other costs. These could be fees or costs related to the loan.

Why Are They Different?

The two rates differ because APR includes more than just interest. It reflects the total cost of borrowing.

Comparison Table: Note Rate vs APR

| Note Rate | APR |

|---|---|

| Interest rate used for monthly payments. | Overall cost of the loan per year, including fees. |

| Does not include fees and other costs. | Includes note rate, fees, and indirect costs. |

| Used for the loan’s principal balance. | Helps compare total loan costs. |

Why Does APR Matter?

APR matters because it shows the true cost of your loan. It helps you compare different loans.

How to Find the Best Loan

Look at both the Note Rate and APR. Choose the loan that has the best overall cost for you.

Example:

Imagine two loans with the same Note Rate. One has a lower APR. This means the second loan has lower costs overall.

Why Understanding These Rates is Crucial for Borrowers

Impact on Monthly Payments

Understanding the difference between Note Rate and APR can significantly impact your monthly mortgage payments. A lower Note Rate means lower monthly payments, but a higher APR could indicate that you’re paying more in fees and other charges, which could offset the benefits of a lower Note Rate.

Long-term Financial Implications

While the Note Rate affects your monthly payments, the APR provides a broader view of the loan’s total cost. A higher APR could mean you’re paying more over the life of the loan, even if the Note Rate is lower. This is because the APR includes all the costs associated with obtaining the loan, not just the interest rate.

How to Compare Note Rate and APR When Shopping for Loans

Tips for Comparing Different Loan Offers

When comparing loan offers, consider both the Note Rate and APR. A loan with a lower Note Rate may seem more attractive, but if the APR is higher, it could mean you’re paying more in the long run.

Questions to Ask Lenders

Ask lenders about the Note Rate and APR for each loan offer. Ensure you understand all the fees and charges included in the APR, so you can make an informed decision.

Common Misconceptions About Note Rate and APR

Clarifying Common Confusions

Some borrowers mistakenly believe that the Note Rate and APR are interchangeable, but they serve different purposes. Others may think that a lower Note Rate always means a better deal, but the APR provides a more comprehensive view of the loan’s cost.

Real-world Examples: Note Rate vs. APR in Action

Example Scenarios

Consider two loan offers with the same Note Rate but different APRs. Loan A has a Note Rate of 4% and an APR of 4.25%, while Loan B has a Note Rate of 4% and an APR of 4.5%. Although the Note Rates are the same, the APRs indicate that Loan B has higher fees and charges, making it more expensive in the long run.

Expert Advice on Choosing Between Different APR and Note Rate Offers

What Experts Say

Financial experts recommend comparing both the Note Rate and APR when shopping for loans. They also suggest asking lenders about any additional fees or charges not included in the APR to get a complete picture of the loan’s cost.

Best Practices for Decision Making

When comparing loan offers, consider the Note Rate and APR, as well as the loan’s terms and conditions. Choose the loan that best aligns with your financial goals and long-term plans.

Frequently Asked Questions of Note Rate vs Annual Percentage Rate

What Determines Note Rate?

Note rate, also known as nominal rate, is determined by the loan’s interest rate without taking into account compounding or any fees.

How Does Apr Differ From Note Rate?

APR, or Annual Percentage Rate, includes both the interest rate and any additional fees or costs, offering a more comprehensive cost of borrowing.

Can Note Rate Affect Monthly Payments?

Absolutely, the note rate directly impacts the monthly payment amount for a loan, with higher rates leading to higher payments.

What’s Included In Apr Calculations?

APR calculations encompass the interest rate plus any additional fees such as broker fees, closing costs, rebates, and discount points.

Conclusion

Note Rate and APR are both important. They help you understand loan costs. Knowing the difference can save you money.

Quick Tips

- Always check both Note Rate and APR when comparing loans.

- APR includes fees and costs, so it’s higher than the Note Rate.

- The lower the APR, the lower your costs over the life of the loan.

Summary

In summary, Note Rate is the interest rate used to calculate your loan payments. APR includes this rate and all other costs of your loan. Knowing these terms helps you make smart loan choices.

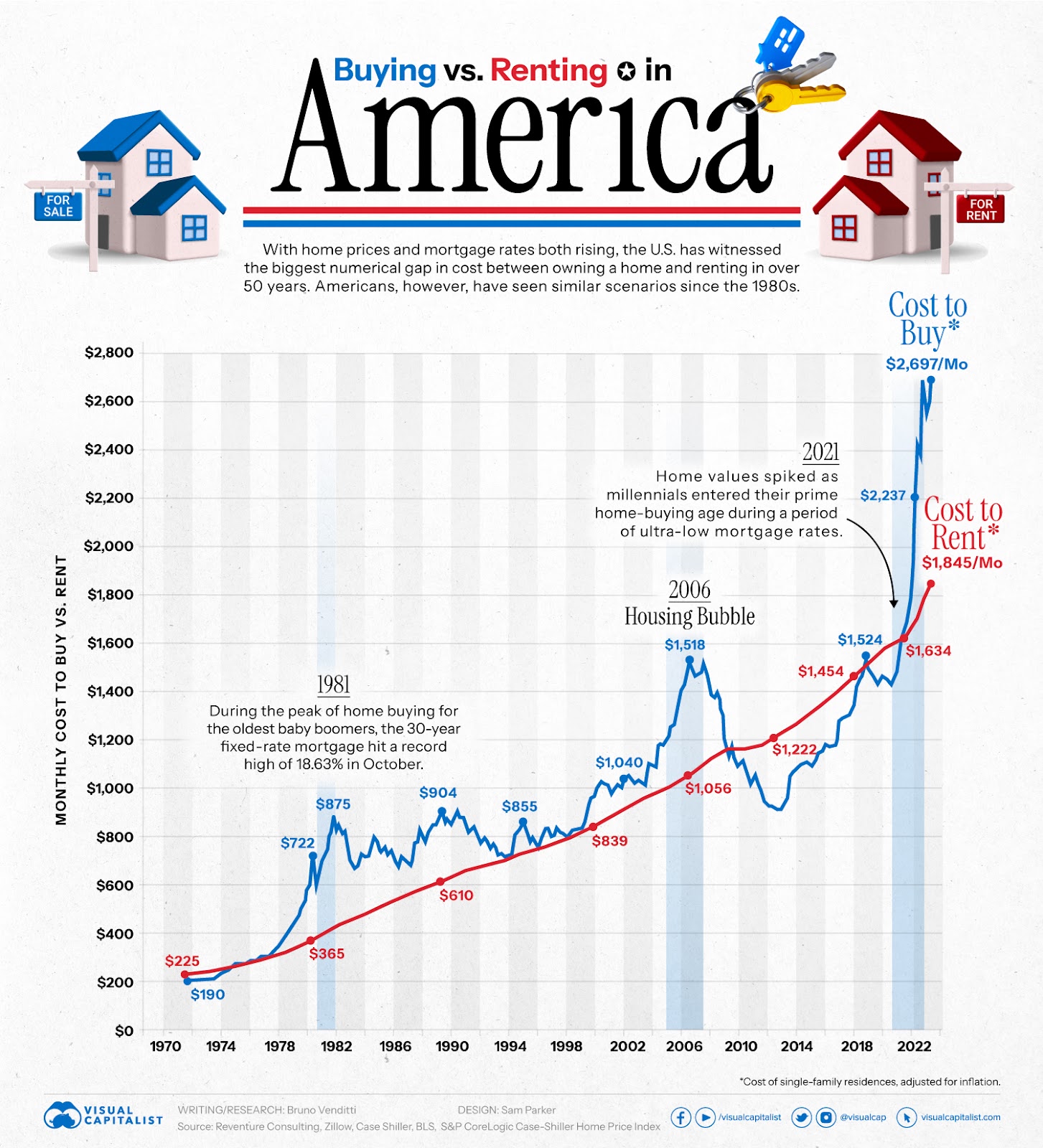

Credit: www.visualcapitalist.com

Need Help?

If you need help understanding your loan options, talk to a loan advisor. They can help you find the best rate for your needs.