Student loans can affect mortgage approval by increasing your debt-to-income ratio (DTI). Lenders scrutinize this ratio to determine your ability to repay a home loan.

Securing a mortgage while managing student loan debt demands a balanced understanding of how lenders evaluate your financial health. Your student loans are a critical part of your credit history, and they can either hinder or help your case. A consistent repayment record can demonstrate financial reliability, making you an attractive candidate to mortgage lenders.

Helping People Achieve Their Dream Of Homeownership!

👉 Simone Castello MLO (NMLS: 2181703)

📧 scastello@certifiedhomeloans.com

📞 WhatsApp No: +1 954-483-7742

Conversely, high student loan balances can inflate your DTI, potentially making you a riskier bet for lenders. Prospective home buyers must navigate these waters carefully to ensure that their education debt does not stand in the way of owning a home. Tailoring your finances to meet lender expectations involves lowering debts and showcasing a stable income, which are pivotal steps towards mortgage approval.

Table of Contents

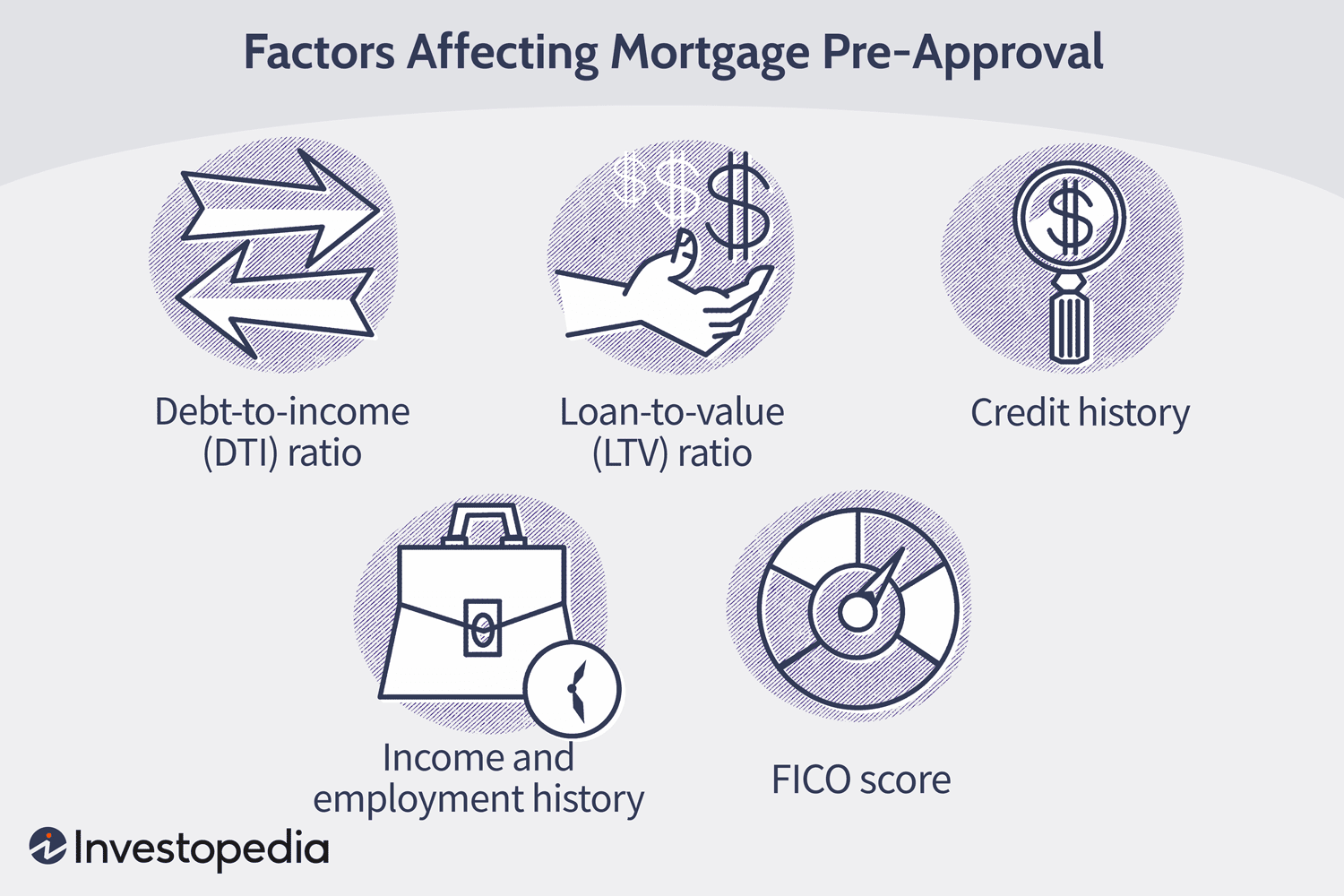

Impact Of Student Loans On Mortgage Eligibility

Understanding how your student loans affect your chance to own a home is crucial. Lenders look at your debt and income to decide if they can give you a mortgage. Let’s break down how student loans can influence this decision.

Debt-to-income Ratio Considerations

Lenders compare your monthly debt to your income before saying yes to a mortgage. This is called your debt-to-income ratio (DTI). If student loans take up a big part of your income, this ratio goes up. A high DTI can make getting a mortgage hard. Here’s why:

- A lower DTI means more trust from lenders. It shows you can handle your money well.

- Big student loans might make your DTI high and reduce how much you can borrow for a house.

Keep your DTI low for a better chance at a good mortgage.

Credit Score Implications

Your credit score is a big deal for lenders. It shows if you’ve been good with money in the past. Student loans can affect this score. Here’s what you need to know:

| Payment History | Credit Utilization | Credit History Length |

|---|---|---|

| Do you pay on time? Good habits boost your score. | Using less of your credit looks good to lenders. | A long history of managing loans can help your score. |

Paying your student loans on time can actually help your credit score grow. Missing payments does the opposite and can dent your chances of getting a house loan.

Qualifying For A Mortgage With Student Debt

Entering the world of home ownership is a thrilling step. But when student loans loom large in your financial profile, you may wonder about the impact on mortgage approval. Understanding the interplay between student debt and mortgage qualification is key to making an informed decision.

Income Stability And Job History

Steady income and a solid job record are crucial for mortgage success. Lenders look for consistency in your earnings. This proves your ability to make monthly payments on time. Let’s break down what counts:

- Two-year work history: Showing employment stability.

- Pay raise prospects: Future earning potential can play to your favor.

- Gaps in employment: Explainable interruptions are often acceptable.

To strengthen your case, document your financial situation thoroughly. Provide pay stubs, tax returns, and employment letters.

Loan Programs For Borrowers With Student Loans

Fortunately, specific loan programs exist to help student loan borrowers secure a mortgage. These programs often consider student debt differently.

| Loan Program | Features |

|---|---|

| FHA Loans | Lower down payments, flexible debt-to-income ratios |

| USDA Loans | No down payment, unique student loan considerations |

| VA Loans | For veterans, few requirements related to student loans |

| Conventional Loans | Focused on overall debt, not just student loans |

Each program offers distinct advantages. Understanding their criteria could increase your chances of approval. Your mortgage advisor will be an invaluable resource in navigating these options.

Strategies To Enhance Mortgage Approval Odds

Getting a mortgage with student loans is tricky, but not impossible. A clear approach can increase the chances of getting that dream home. Understand these strategies to better the odds of approval. Starting with how to handle existing student loans is key.

Paying Down Student Loans

Mortgage lenders assess debt-to-income ratio (DTI). Lower DTI means better chances for approval. Work towards reducing student loan balances. Regular, on-time payments show responsibility.

Include the following tactics:

- Extra payments: Apply bonuses or tax refunds to student loans.

- Smaller savings: Temporarily reduce retirement savings to pay down student debt.

- Budget adjustments: Cut unnecessary expenses to free up more money for loan payments.

Consolidation And Refinancing Options

Explore consolidation or refinancing. Both options might lower monthly payments and interest rates.

Consider these points when choosing:

| Consolidation | Refinancing |

|---|---|

| Combines multiple loans into one | Replaces current loan with new, often lower-rate loan |

| May offer federal loan benefits | Best for high-interest private loans |

| Federal programs offer income-driven repayment plans | Requires solid credit score |

Before deciding, calculate the long-term costs. Speak with loan specialists who can provide tailored advice.

Credit: www.investopedia.com

Understanding Different Types Of Mortgages

Getting a mortgage is like setting sail on a new adventure. Before setting off, it’s important to know the types of ships available. Similarly, understanding different types of mortgages prepares you for smoother sailing towards homeownership, even with student loans as part of your cargo.

Conventional Vs. Government-insured Loans

Conventional loans are the most common. They’re like the sturdy boats of the mortgage sea. Lenders give these without government backing.

- These loans often need a higher credit score.

- A down payment is usually necessary.

- Having student loans may impact the loan-to-income ratio.

Government-insured loans offer a safety net. They are like lifeboats provided by the government. Three types are:

- FHA loans: Backed by the Federal Housing Administration. Good for those with student loans and a smaller down payment. Read the Pros and Cons of an FHA Loan

- VA loans: For veterans and service members. They offer perks like no down payment, even with student debt.

- USDA loans: For rural home buyers. These also have lenient terms for those with student loans.

Fixed-Rate and Adjustable-Rate Mortgages

A fixed-rate mortgage is like a dependable rowboat. The interest rate stays the same.

- Payments are predictable.

- Student loans won’t affect your interest.

An adjustable-rate mortgage (ARM) is more like a sailboat. It catches the wind and the rate may change.

- The initial rate is often lower but can adjust later.

- Budgeting can be tricky with student loans and a changing rate.

| Mortgage Type | Interest Type | Pros | Cons |

|---|---|---|---|

| Fixed-Rate | Unchanging | Predictable payments | Potentially higher initial rates |

| ARM | Variable | Lower initial rates | Uncertainty in long-term |

Navigating The Mortgage Application Process

Entering the world of mortgages brings a myriad of factors into play. Student loans can be one of them. Understanding their impact is key during the mortgage application process.

Documenting Income And Debt

Lenders look at your debts and income. They need proof to make decisions.

Bold documents are often needed:

- Pay stubs: Show recent earnings.

- W-2 forms and tax returns: Reflect annual income.

- Student loan statements: Reveal monthly payments.

- Credit report: Lists all debts and payment history.

Your debt-to-income (DTI) ratio becomes crucial. Loans affect your DTI. High DTI can hurt mortgage chances.

Effect of Student Loan Deferral or Forgiveness

| Income | Monthly Debts | DTI Ratio |

|---|---|---|

| $5,000 | $1,500 (including student loans) | 30% |

Mortgages get tricky with deferred student loans. Lenders may count them differently. A deferral means payments are not due yet. Lenders still consider these loans.

Some may use:

- A percentage of the loan balance.

- Payment amounts listed on the credit report.

Loan forgiveness can be a relief. It reduces debt and may help your DTI ratio. But you need to prove it to lenders.

Provide the lender with:

- Forgiveness program documents: Show eligibility and terms.

- Written confirmation: Proves loans will be forgiven.

Clear explanations ensure lenders understand your financial position.

Expert Tips For Managing Student Loans And Home Buying

Welcome to ‘Expert Tips for Managing Student Loans and Home Buying’. Navigating the journey toward homeownership is thrilling. Simultaneously managing student loans can be challenging. Understanding how these loans impact mortgage approval is crucial. This guide offers key strategies to balance both financial commitments effectively.

Financial Planning And Budgeting

Meticulous financial planning forms the cornerstone of managing both student debt and the home buying process. Start by evaluating your current financial health. Draft a budget that includes all debt obligations alongside anticipated mortgage payments.

- Analyze monthly income versus expenditures to understand available funds for a mortgage.

- Create a savings plan for a down payment without neglecting student loan payments.

- Utilize debt-to-income ratio calculations to gauge loan affordability.

- Explore loan repayment plans that might lower monthly student loan payments.

Automating payments ensures all debts are paid on time, enhancing credit scores. This strategy demonstrates financial responsibility to mortgage lenders.

Seeking Advice From Mortgage Professionals

Professional insight is invaluable in the home buying process. Mortgage professionals offer personalized advice based on your unique financial situation.

- Consult with loan officers to understand mortgage options compatible with your student loan status.

- Pre-approval for a mortgage provides clarity on the price range and bolsters bargaining power with sellers.

- Discuss down payment assistance programs, which might alleviate initial financial stress.

- Acknowledge the impact of student loans on credit scores and seek strategies to maintain or improve your rating.

Keep in mind, communication with lenders about your student loans presents a transparent financial picture. Transparency fosters trust and may positively influence the mortgage process.

Remember, balancing student loans with the pursuit of homeownership demands careful planning and informed decision-making.

Credit: www.credit.com

Frequently Asked Questions On How Student Loans Affect Your Mortgage Approval

Do Student Loans Impact Mortgage Eligibility?

Yes, student loans can impact mortgage eligibility. Lenders consider your debt-to-income ratio (DTI), which includes student loan payments. A high DTI can reduce your loan amount or hinder approval chances.

How Does Loan Deferment Affect Mortgage Approval?

Loan deferment can affect mortgage approval by impacting your debt-to-income ratio. While payments are paused, lenders still consider the potential future payments in calculating your DTI, potentially affecting loan terms.

Can Consolidating Student Loans Help With Mortgage Approval?

Consolidating student loans may help with mortgage approval. It can simplify debt management and potentially lower monthly payments, which may improve your debt-to-income ratio, a key factor in mortgage considerations.

What Credit Score Do I Need For A Mortgage With Student Loans?

The credit score needed can vary, but generally, a score of 620 or higher is sought for conventional loans. However, having student loans might require a higher score to counterbalance your debt levels.

Conclusion

Navigating the mortgage process amidst student loan debt requires informed strategies. A solid credit score and manageable debt-to-income ratio are your allies. Remember, proper financial planning and understanding lender criteria can bridge the gap between student loans and home ownership dreams.

Start preparing now for a smoother mortgage approval journey.